| Best workplaces for commutersChanging How America Commutes |

qualified transportation fringe benefits

(Last Updated on 1/8/2024)

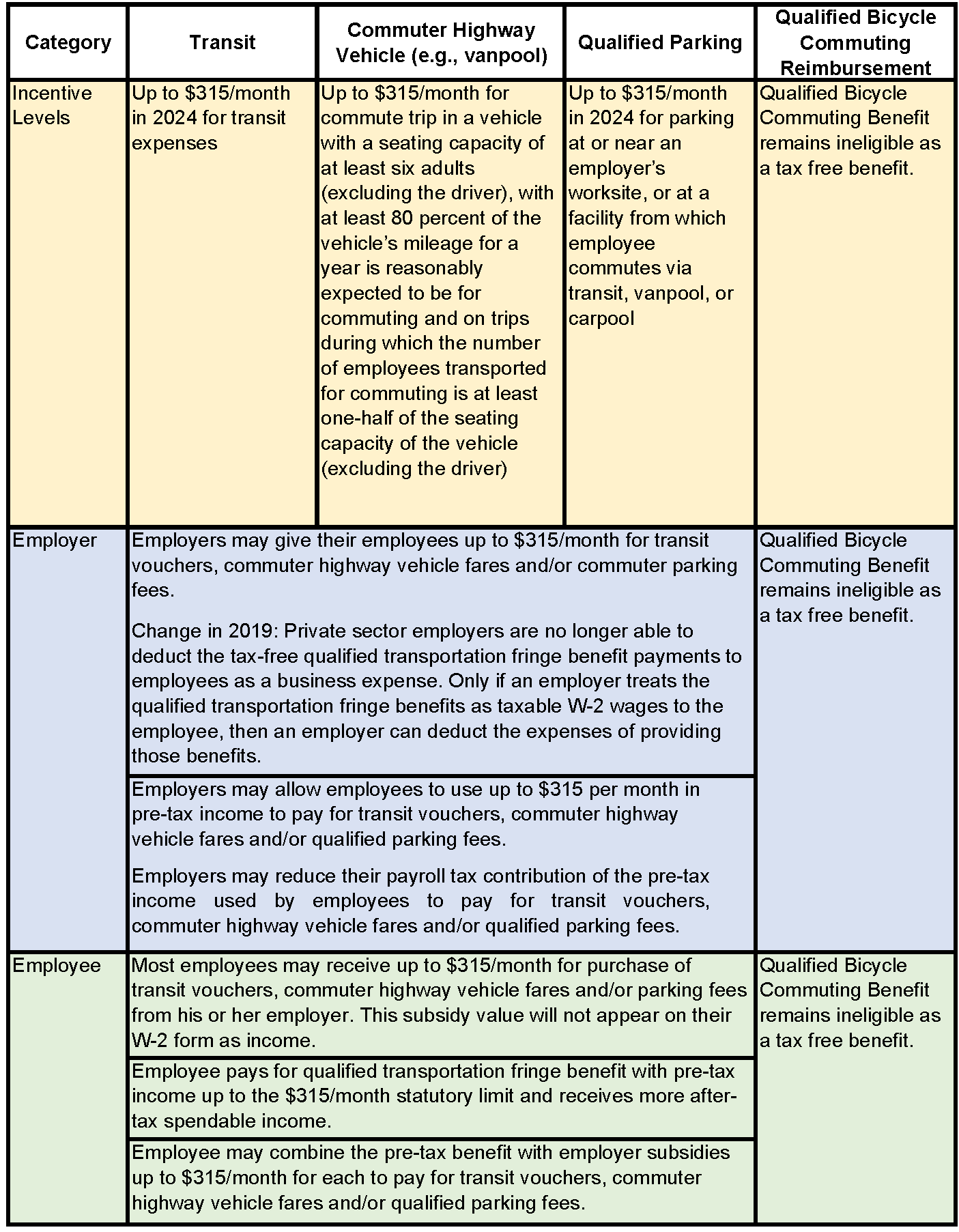

IRS Revenue Procedure 2023-34 raised the qualified transportation fringe benefit monthly limitation from $300 in 2023 to $315 in 2024. The monthly limitation under § 132(f)(2)(A) regarding the aggregate fringe benefit exclusion amount for transportation in a commuter highway vehicle and any transit pass is $315. The monthly limitation under § 132(f)(2)(B) regarding the fringe benefit exclusion amount for qualified parking is $315.

See the summary table below.

Qualified bicycle commuting reimbursements, previously allowed up to $240 per year prior to 2018, remains ineligible in 2024 as a tax-free benefit. Employers may continue to provide the bicycle benefit as a taxable benefit.

On June 23, 2020, the Internal Revenue Service issued proposed regulations (IR-2020-125) that provide guidance for the deduction of qualified transportation fringe and commuting expenses. According to the IRS, “The Tax Cuts and Jobs Act (TCJA) does not allow deductions for qualified transportation fringe (QTF) expenses and does not allow deductions for certain expenses of transportation and commuting between an employee’s residence and place of employment.”

The law also provided that a tax-exempt organization’s unrelated business taxable income (UBTI) is increased by the amount of the QTF expense that is nondeductible. However, on December 20, 2019, this was repealed as part of the Further Consolidated Appropriations Act of 2020. This repeal was retroactive to the original date of enactment by the TCJA.

These proposed regulations specifically address the elimination of the deduction for expenses related to QTFs provided to an employee of the taxpayer. The proposed regulations also provide guidance and methodologies to determine the amount of QTF parking expense that is nondeductible. The guidance also includes definitions and special rules to clarify and simplify the calculations underlying the methodologies.

Please consult your tax professional for guidance in complying with the TCJA requirements and the subsequent guidance.

Employers that subsidize at least $30 per month for transit or vanpool fares may meet the National Standard of Excellence and qualify for designation under Best Workplaces for Commuters.

|

| 2023 Commuter Benefits Guide for Employers

Your essential guide to setting up and carrying out a successful commuter benefit program. From determining what commuter benefits are eligible for providing tax free to employees to customizing the program for your circumstances, this e-book will guide you through the options available to effectively provide your employees with a commuter benefits program. Employers can leverage employer-provided benefits to yield happier employees, support more sustainable employee commute behavior, and generate tax savings for employees and the employer. |

Summary Table

* tax free transit and vanpool benefit limit was increased to $315 per month for 2024.

* tax free parking benefit limit was increased to $315 per month beginning on January 1, 2024.

Frequently Asked Questions

According to the Internal Revenue Code Section 132(f), employer-paid reimbursements or payments for qualified commuter benefits are excludable from income for purposes of taxation. The following frequently asked questions were extracted from IRS documentation and updated to reflect the 2023 limits on Qualified Transportation Fringe Benefits (QTFB) and recent changes to the Tax Cuts and Jobs Act.

Disclaimer: Best Workplaces for Commuters does not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting professionals before engaging in any qualified transportation fringe benefit program.

Answer

Transit passes include any vouchers, passes, farecards, tokens, or related items that employees can use to pay for transportation on mass transit facilities or transportation provided by a person in the business of transporting persons for compensation or hire if such transportation has a seating capacity of at least six adults (not including the driver). Transit agency “smart cards” are also included.

Answer

IRS Code Section 132(f) defines transportation in a commuter highway vehicle as: Transportation provided by an employer to an employee in connection with travel between the employee’s residence and place of employment. A commuter highway vehicle is a highway vehicle with a seating capacity of at least six adults (excluding the driver) and with respect to which at least 80 percent of the vehicle’s mileage for a year is reasonably expected to be— (a) For transporting employees in connection with travel between their residences and their place of employment; and (b) On trips during which the number of employees transported for commuting is at least one-half of the adult seating capacity of the vehicle (excluding the driver). Section 132(f) is generally viewed as applying to vanpools, but large carpools could be eligible as well. Based on the definition above, any 7-passenger vehicle (e.g., large SUV) with 4 riders and meeting the 80 percent mileage requirement would qualify.

Answer

The IRS defines qualified parking as parking provided to an employee by an employer on or near the employer’s business premises or at a location from which the employee commutes to work (such as a park-and-ride lot) by commuter highway vehicle or carpool. Qualified parking does not include the value of parking provided to an employee that is excludable from gross income as a working condition fringe benefit. It also does not include reimbursement paid to an employee for parking costs that are excludable from gross income as an amount treated as paid under an accountable plan, such as if the employer provides parking on property that the employer owns or leases; the employer pays for the parking; or the employer reimburses the employee for parking expenses. Parking on or near property used by the employee for residential purposes is not qualified parking.

Answer

No. The Tax Cuts and Jobs Act amended Section 132(f) to suspend the qualified bicycle commuting reimbursement provision for any taxable year beginning after December 31, 2017, and before January 1, 2026.

Answer

No. The Tax Cuts and Jobs Act also eliminated the ability of employers to deduct employer-provided tax-free QTFBs (e.g., subsidized transit fare, parking costs, and commuter highway vehicles payments) as ordinary business expense. The Act states that, beginning in 2018, ‘No deduction shall be allowed under this chapter for the expense of any qualified transportation fringe (as defined in section 132(f)) provided to an employee of the taxpayer… No deduction shall be allowed under this chapter for any expense incurred for providing any transportation, or any payment or reimbursement, to an employee of the taxpayer in connection with travel between the employee’s residence and place of employment, except as necessary for ensuring the safety of the employee.’ On June 23, 2020, the Internal Revenue Service issued proposed regulations (IR-2020-125) that provide guidance for the deduction of qualified transportation fringe and commuting expenses. According to the IRS, “The Tax Cuts and Jobs Act (TCJA) does not allow deductions for qualified transportation fringe (QTF) expenses and does not allow deductions for certain expenses of transportation and commuting between an employee’s residence and place of employment.” BWC Commentary: We recommend employers refer to the IRS Publication 15B once it is published in 2021 to confirm the above interpretation.

Answer

Section 132(f)(5)(E) states that self-employed individuals who are employees within the meaning of section 401(c)(1) are not employees for purposes of section 132(f). Therefore, individuals who are partners, sole proprietors, or other independent contractors are not employees for purposes of section 132(f). In addition, under section 132(a), 2% shareholders of S corporations are treated as partners for fringe benefit purposes. Thus, an individual who is both a 2% shareholder of an S corporation and a common law employee of that S corporation is not considered an employee for purposes of section 132(f). However, while section 132(f) does not apply to individuals who are partners, 2% shareholders of S corporations, or independent contractors, other exclusions for working condition and de minimis fringes may be available.

Answer

No. Section 132(f) does not require that a Qualified Transportation Fringe Benefit plan be in writing.

Answer

There are no substantiation requirements if the employer distributes transit passes. Thus, an employer may distribute a transit pass for each month with a value not more than the statutory monthly limit without requiring any certification from the employee regarding the use of the transit pass. However, an employer may choose to impose more substantiation requirements.

Answer

Generally, carpools are ineligible to receive federal commuter benefits unless the carpool meets the definition of a commuter highway vehicle. That means the vehicle being used must provide transportation in connection with travel between the employee’s residence and place of employment. A commuter highway vehicle is a highway vehicle with a seating capacity of at least six adults (excluding the driver) and with respect to which at least 80% of the vehicle’s mileage for a year is reasonably expected to be for transporting employees in connection with travel between their residences and their place of employment and on trips during which the number of employees transported for commuting is at least one-half of the adult seating capacity of the vehicle (excluding the driver). In other words, it must be at least a four-person carpool in a large seven-passenger vehicle like a minivan, SUV or crossover. BWC Commentary: You may wish to consult your state statutes for as to how “vanpool” is defined to determine if there are any differences in the definition that would determine the treatment of such benefits for state tax purposes.

Answer

Yes. Under Section 132(f), Qualified Transportation Fringe Benefits, an employee may carry over unused compensation reduction amounts to subsequent periods under the plan of the employee’s employer. The following example illustrates this principle. By an election made before November 1 of a year for which the statutory monthly mass transit limit is $300, Employee E elects to reduce compensation in the amount of $300 for the month of November. Employee E incurs $250 in employee-operated commuter highway vehicle expenses during November, for which Employee E is reimbursed $250 by Employer R, Employee E’s employer. By an election made before December, Employee E elects to reduce compensation by $300 for the month of December. Employee E incurs $300 in employee-operated commuter highway vehicle expenses during December for which Employee E is reimbursed $300 by Employer R. Before the following January, Employee E elects to reduce compensation by $250 for the month of January. Employee E incurs $300 in employee-operated commuter highway vehicle expenses during January for which Employee E is reimbursed $300 by Employer R because Employer R allows Employee E to carry over to the next year the $50 amount by which the compensation reductions for November and December exceeded the employee-operated commuter highway vehicle expenses incurred during those months. In this example, because Employee E is reimbursed in an amount not exceeding the applicable statutory monthly limit, and the reimbursement does not exceed the amount of employee-operated commuter highway vehicle expenses incurred during the month of January, the amount reimbursed ($300) is excludable from Employee E’s wages for income and employment tax purposes.

Answer

For purposes of the special rule above, a transit system voucher is an instrument that may be purchased by employers from a voucher provider that is accepted by one or more mass transit operators (e.g., train, subway, bus) in an area as fare media or in exchange for fare media. Thus, for example, a transit pass that may be purchased by employers directly from a voucher provider is a transit system voucher. The term voucher provider means any person in the trade or business of selling transit system vouchers to employers or any transit system or transit operator that sells vouchers to employers for the purpose of direct distribution to employees. Thus, a transit operator might or might not be a voucher provider. A voucher provider is not, for example, a third-party employee benefits administrator that administers a transit pass benefit program for an employer using vouchers that the employer could obtain directly.

Answer

Fare media charges relate only to fees paid by the employer to voucher providers for vouchers. The determination of whether obtaining a voucher would result in fare media charges that cause vouchers to not be readily available as described above is made with respect to each transit system voucher. If more than one transit system voucher is available for direct distribution to employees, the employer must consider the fees imposed for the lowest cost monthly voucher for purposes of determining whether the fees imposed by the voucher provider satisfy this paragraph. However, if transit system vouchers for multiple transit systems are required in an area to meet the transit needs of the individual employees in that area, the employer has the option of averaging the costs applied to each transit system voucher for purposes of determining whether the fare media charges for transit system vouchers satisfy this paragraph. Fare media charges are described in this paragraph and therefore cause vouchers to not be readily available if and only if the average annual fare media charges that the employer reasonably expects to incur for transit system vouchers purchased from the voucher provider (disregarding reasonable and customary delivery charges imposed by the voucher provider, e.g., not in excess of $15) are more than 1% of the average annual value of the vouchers for a transit system.

Answer

Yes. See below for examples.

Answer

Advance purchase requirements cause vouchers to not be readily available only if the voucher provider does not offer vouchers at regular intervals or fails to provide the voucher within a reasonable period after receiving payment for the voucher. For example, a requirement that vouchers may be purchased only once per year may effectively prevent an employer from obtaining vouchers for distribution to employees. An advance purchase requirement that vouchers be purchased not more frequently than monthly does not effectively prevent the employer from obtaining vouchers for distribution to employees.

Answer

Purchase quantity requirements cause vouchers to not be readily available if the voucher provider does not offer vouchers in quantities that are reasonably appropriate to the number of the employer’s employees who use mass transportation (for example, the voucher provider requires a $1,000 minimum purchase and the employer seeks to purchase only $200 of vouchers).

Answer

If the voucher provider does not offer vouchers in denominations appropriate for distribution to the employer’s employees, vouchers are not readily available. For example, vouchers provided in $5 increments up to the monthly limit are appropriate for distribution to employees, while vouchers available only in a denomination equal to the monthly limit are not appropriate for distribution to employees if the amount of the benefit provided to the employer’s employees each month is normally less than the monthly limit.

Answer

Employers that make cash reimbursements must establish a bona fide reimbursement arrangement to establish that their employees have, in fact, incurred expenses for transportation in a commuter highway vehicle, transit passes, or qualified parking. For purposes of section 132(f), whether cash reimbursements are made under a bona fide reimbursement arrangement may vary depending on the facts and circumstances, including the method or methods of payment utilized within the mass transit system. The employer must implement reasonable procedures to ensure that an amount equal to the reimbursement was incurred for transportation in a commuter highway vehicle, transit passes, or qualified parking. The expense must be substantiated within a reasonable period of time. An expense substantiated to the payor within 180 days after it has been paid will be treated as having been substantiated within a reasonable period of time. An employee certification at the time of reimbursement in either written or electronic form may be a reasonable reimbursement procedure depending on the facts and circumstances.

Answer

Yes.

Answer

Yes. An employer may provide benefits of any amount, or provide no assistance, in the purchase of vouchers.

Answer

In general, the value of transit passes provided in advance to an employee for a month in which the individual is not an employee must be included in the employee’s wages for income tax purposes. Transit passes distributed in advance to an employee are excludable from wages for income and employment tax withholding purposes if the employer distributes transit passes to the employee in advance for not more than three months. At the time the passes are distributed, there cannot be an established date that the employee’s employment will terminate (for example, if the employee has given notice of retirement) occurring before the beginning of the last month of the period for which the transit passes are provided. Assume the employer distributes transit passes quarterly, and the employee elects to have $840 deducted from salary to cover transit vouchers for April, May, and June. If employment terminates on May 31, and there was not an established date of termination at the time the transit passes were distributed, then the value of the transit passes provided for June ($300) is excludable from the employee’s wages for employment tax purposes. However, the value of the transit passes distributed for June ($300) is not excludable from wages for income tax purposes. If the employee’s termination date was established at the time the transit passes were provided, then the $300 is included in the employee’s wages for both income and employment tax purposes.

Answer

The most common internal administrative costs faced by employers who implement QTFB programs include the cost of managing the program on a day-to-day basis, marketing the program to employees, distributing transit passes or vouchers, etc. Other internal costs depend on the type of program that the employer chooses to establish. For example, if an employer sets up a vanpool program, then typical costs could include the amount of money spent on purchasing or leasing a commuter highway vehicle, finding and/or training someone to drive the vehicle, and any additional insurance expenses.

Answer

No. The Internal Revenue Code does not require that a commuter benefits plan be in writing or that any form of written plan be submitted to the IRS. However, a company may wish to have certain written rules in order to answer employee questions and describe how the commuter benefit program operates. For example, an employer could write a plan that describes: • Which employees are eligible to receive commuter benefits • What benefits will be provided by the company • How the company vanpool and emergency ride home programs operate • The procedure for enrolling in and discontinuing participation in the benefits program The company should not submit this plan to the IRS, but should make it available to all employees.

Answer

Qualified commuter benefits that do not exceed the statutory monthly limit are not considered wages for purposes of FICA, the Federal Unemployment Tax Act (FUTA), and federal income tax withholding. Any amount by which an employee elects to reduce compensation under the limit is not subject to the FICA, the FUTA, and federal income tax withholding. Qualified commuter benefits exceeding the applicable statutory monthly limit are wages for purposes of FICA, FUTA, and federal income tax withholding and are reported on the employee’s Form W-2, Wage and Tax Statement. Also, cash reimbursements to employees (for example, cash reimbursement for qualified parking) in excess of the applicable statutory monthly limit are treated as paid for employment tax purposes when actually or constructively paid. Employers must report and deposit the amounts withheld in addition to reporting and depositing other employment taxes. To receive payroll tax savings, employees do not have any additional paperwork requirements beyond those normally performed when filing taxes.

Answer

No. With increased availability of electronic fare media on transit systems, the IRS announced that after December 31, 2015, employers will no longer be permitted to provide Qualified Transportation Fringe Benefits in the form of cash reimbursement in geographic areas where terminal-restricted debit cards are readily available (Rev. Rul. 2014-32).

Answer

Smartcards are cards that contain a memory chip storing certain information that uniquely identifies the card and value stored on the card, and that can be used either as fare media or to purchase fare media. The amount stored on the smartcard provided by a transit system must be usable only as fare media; it cannot be used for any other purpose or to purchase anything else. Of course, the amount cannot exceed the statutory limit (currently $300 per month). The employer makes payments directly to the transit system and instructs how much should be placed on each employee’s smartcard. The employer does not require employees to substantiate their use of the cards.

Answer

Terminal-restricted debit cards are debit cards that are restricted for use only at merchant terminals at points of sale at which only fare media for local transit systems is sold.

Answer

The employer must provide a debit card that is restricted for use only at merchant terminals at points of sale at which only fare media for the transit systems are sold. The other conditions for using a terminal-restricted debit card are similar to those governing the use of a smartcard.

Answer

In most communities, your employer is not required to provide Qualified Transportation Fringe Benefits or offer the opportunity for employees to use pre-tax income to purchase fare media. However, your employer must be involved in either offering subsidies or allowing you to purchase are media with pre-tax income for you to exclude those benefits from wages for FICA, FUTA, and income tax withholding under section 132(f).

Answer

The Tax Cuts and Jobs Act required qualified transportation fringe benefits provided by an employer to be treated as a non-deductible expense by the employer effective for amounts paid or incurred after December 31, 2017. If an employer pays a third party to provide qualified parking, for example, then the final regulations generally treat the employer's total annual cost paid to the third party as the amount of the employer's deduction disallowance. The regulations required taxpayers to use the expense paid or incurred in providing a qualified transportation fringe benefit and not its value to an employee, allocate parking expenses to reserved employee spaces, and properly apply the exception for parking made available to the general public. See Qualified Transportation Fringe, Transportation and Commuting Expenses Final Rule posted on Dec 16, 2020 for more information.

additional resources2023 Commuter Benefits for Employers Guide e-book Publication 15B, Employer’s Tax Guide to Fringe Benefits: Transportation (Commuting) Benefits http://www.irs.gov/publications/p15b/index.html Fringe Benefits Guide https://www.irs.gov/pub/irs-pdf/p5137.pdf Qualified Transportation Fringe Benefits https://www.federalregister.gov/documents/2001/01/11/01-294/qualified-transportation-fringe-benefits Rev. Rul. 2014-32 https://www.irs.gov/pub/irs-drop/rr-14-32.pdf Qualified Transportation Fringe, Transportation and Commuting Expenses (December 16, 2020) https://www.regulations.gov/document/IRS-2020-0019-0017 Qualified Transportation Fringe, Transportation and Commuting Expenses Under Section 274: Correction https://www.federalregister.gov/documents/2021/04/28/2021-08391/qualified-transportation-fringetransportation-and-commuting-expenses-under-section-274-correction Transportation Impacts of Commuter Benefits The Transit Cooperative Research Program of the Transportation Research Board has published two research studies on commuter benefits: TCRP Report 87—Strategies for Increasing the Effectiveness of Commuter Benefits Programs https://onlinepubs.trb.org/onlinepubs/tcrp/tcrp_rpt_87.pdf TCRP Report 107—Analyzing the Effectiveness of Commuter Benefits Programs |